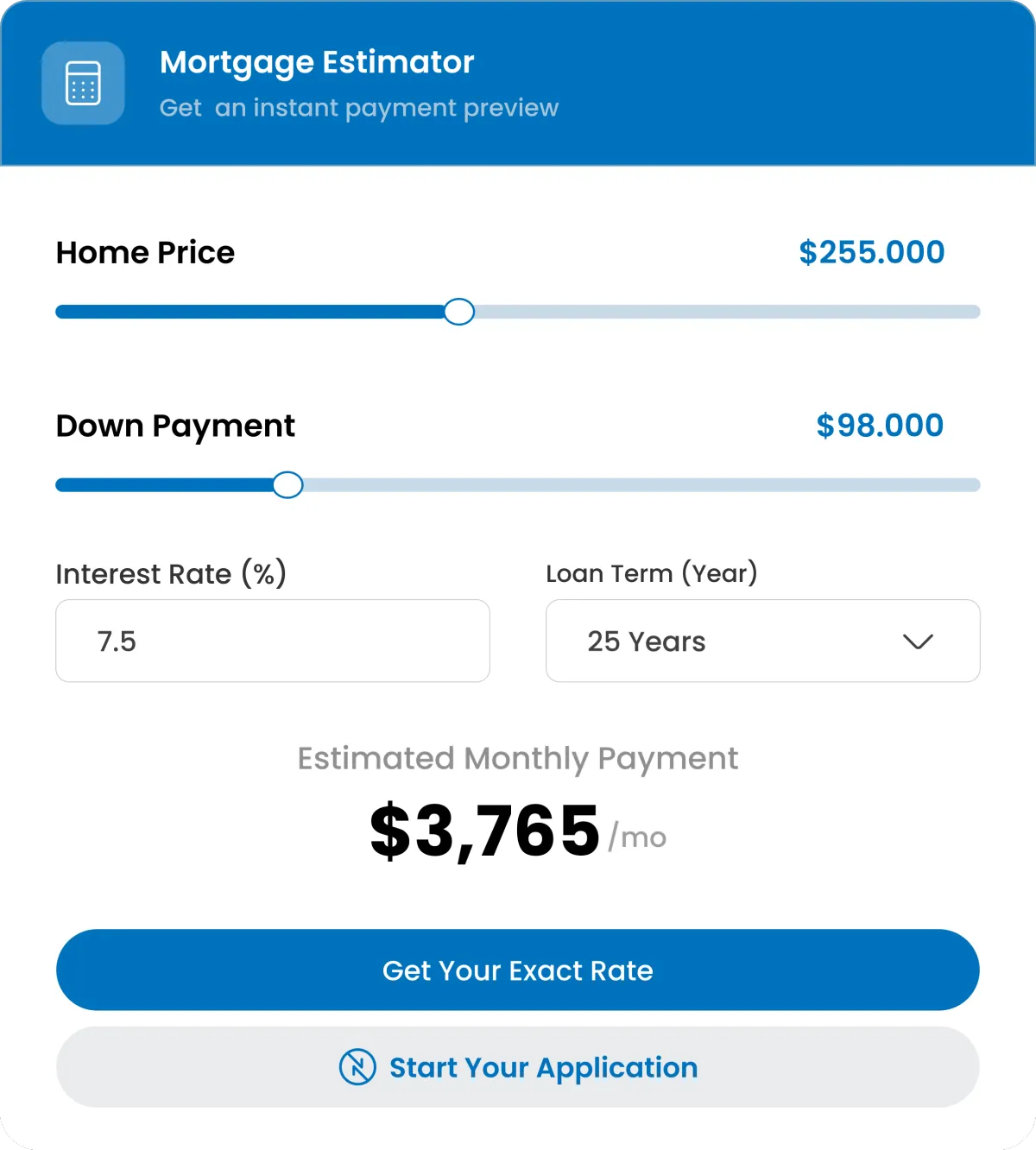

Nextgen Mortgage Calculators

From VA loan benefits to refinance savings, our calculators give you real numbers to help you move forward with clarity.

$0

Always Free

30s

INSTANT RESULTS

98%

ACCURACY RATE

WHY OUR TOOLS

Built for Accuracy, Not Just Estimates

Our calculators use live rate data and VA-specific rule sets — so you get answers you can actually act on.

Live Rate Integration

All calculators pull today's mortgage rates, not outdated defaults. Get a real picture of what you'll actually pay.

VA-Specific Calculations

Built-in VA funding fee tables, entitlement scenarios, and $0 down calculations — no generic tool covers this depth.

No Login Required

Use any calculator instantly. No account, no email, no credit pull — just clear, private, instant numbers.

All Mortgage Calculators

Extra Mortgage Payment Calculator

See exactly how much you save in interest and how many years you cut from your mortgage.

VA Loan Calculator

Free VA loan calculator with automatic funding fee calculation. $0 down, no PMI.

Cash-Out Refinance Calculator

See how much equity you can turn into cash, what your new mortgage payment will look like, and when the refinance pays for itself.

Home Equity Loan Calculator

See how much you can borrow against your home, what your monthly payments will look like, and the total cost over your loan term.

Mobile Home Loan Calculator

See how much you can borrow for a manufactured or mobile home, what your monthly payment will look like, and how loan type affects your total cost.

Seller Closing Costs Calculator

See how much you'll walk away with at closing, what fees and commissions to expect, and how your final net proceeds break down.

FHA Streamline Refinance Calculator

See how much you could save by refinancing your FHA loan, estimate your new monthly payment, and compare your current loan with streamlined refinance options.

Refinance Break Even Calculator

See how long it will take for your monthly savings to cover the cost of refinancing, compare loan options, and determine when refinancing starts saving you money.

VA Loan Mortgage Affordability Calculator

See how much home you may be able to afford with a VA loan, estimate your monthly payment, and understand how loan terms impact your buying power.

Reverse Mortgage Calculator

Estimate how much equity you may be able to access through a reverse mortgage, review payout options, and understand how your loan balance may change over time.

VA Loan DTI Calculator

See how much home you may be able to afford with a VA loan, calculate your debt-to-income ratio, and understand how loan terms impact your monthly payment and buying power.

Bank Statement Loan Calculator

Estimate how much home you may qualify for using bank statement income, calculate your effective monthly income from deposits, and see how it impacts your loan eligibility.

Why Veterans Choose NextGen Mortgage Loans

Built for military families who want honest numbers and real guidance, not hidden fees.

No Information Required

Calculate anonymously, no sign-up needed.

Live Rate Data

Know how much home you can afford.

VA Specialists On Staff

Find the perfect home within your budget.

4.9 / 5 Rating

Work with our team for a smooth closing process.

Ready to Take the Next Step?

Our loan specialists are standing by to walk you through

your numbers and lock in today's best rate.

Client Testimonials

Don't just take our word for it. Hear from the families we've helped

secure their dream homes.

Frequently Asked Question

How much can I save by making extra mortgage payments?

The savings depend on your loan balance, interest rate, and how much extra you pay. For example, adding $200 per month to a $300,000 mortgage at 6.38% can save you over $72,000 in interest and cut roughly 6 years off a 30-year loan. Use the calculator above to see your exact savings.

Should I make extra mortgage payments or invest the money?

It depends on your financial situation. Extra mortgage payments offer a guaranteed return equal to your interest rate with zero risk. If your mortgage rate is 6% or higher, paying it down is a strong choice. However, if you have high-interest debt like credit cards, pay those off first. Consider maxing out tax-advantaged retirement accounts before making extra mortgage payments.

Is it better to pay extra monthly or make a lump sum payment?

Both approaches reduce your balance and save interest, but monthly extra payments typically work better for most people because they build a consistent habit and reduce your principal steadily throughout the year. A lump sum payment is effective if you receive a bonus or inheritance. The key factor is timing: the earlier you make extra payments, the more interest you save.

Do extra mortgage payments go toward the principal?

Yes, when you make an extra payment and specify it as a principal-only payment, the entire amount goes toward reducing your loan balance. This is different from your regular payment, which splits between principal and interest. Always confirm with your lender that extra payments are applied to principal, not future payments.

Are there penalties for paying off a mortgage early?

Most modern mortgages do not have prepayment penalties. FHA loans, VA loans, and loans from federally chartered credit unions prohibit prepayment penalties by law. However, some conventional loans may include a penalty during the first 3 to 5 years. Check your loan agreement or ask your lender before making large extra payments.

How do biweekly mortgage payments work?

Instead of making 12 monthly payments per year, you pay half your monthly amount every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equals 13 full monthly payments. That one extra payment per year can shave several years off your mortgage and save thousands in interest.

Start your Mortgage Loan Pre-Approval.

NextGen Mortgage can issue mortgage loan pre-approvals in as little as 15 minutes.

MLO License Info: NMLS #1621958, NH Broker license #1621958MBRR, and MA Broker license #MB1621958, ME Broker License #1621958, FL Broker License #MBR4542, RI Broker License #20265029LB

Company

Services

Contact